The Korea–Australia Free Trade Agreement (KAFTA) is a comprehensive, world-class agreement that substantially frees up Australia's trade with Korea – our fourth-largest trading partner. The agreement helps level the playing field for Australian exporters competing with those from the United States, the European Union, Chile and the Association of Southeast Asian Nations (ASEAN), who already benefit from trade deals with Korea. Without KAFTA, Australian exporters would continue to face a disadvantage in the Korean market.

KAFTA eliminates or reduces barriers to trade between Korea and Australia. This benefits Australian businesses that want to export Australian goods to Korea or want to import Korean goods to sell in Australia.

Using KAFTA

A common obstacle to importing and exporting goods is tariffs (customs duties) – taxes imposed by governments on goods arriving from overseas. On the day KAFTA entered into force in December 2014, Korean tariffs were set at zero for 84 per cent (by 2013 import value) of Australian exports. This will rise to 95.7 per cent by 2025 and 99.8 per cent once KAFTA is fully implemented. KAFTA also set Australian tariffs at zero on 86 per cent of Korean exports from day one, rising to 100 per cent by 2022.

This step-by-step guide will help Australian importers and exporters to take advantage of preferential tariff treatment under KAFTA by answering the following questions:

What goods am I exporting or importing?

- Identifying the customs tariff code for a good is a critical first step.

How are these goods treated under KAFTA?

- This guide will help you identify the preferential duty rate for your goods.

- Most eligible goods will benefit from a 'preferential' (lower) duty rate under KAFTA.

Where are my goods produced?

- Only goods that 'originate' in Australia or Korea are eligible for preferential tariff treatment under KAFTA. There are specific rules to determine eligibility. This prevents businesses from other countries gaining the benefit of KAFTA by simply transhipping their goods through Australia or Korea.

My goods qualify for preferential treatment under KAFTA. How do I ensure I get the lower tariff rate?

- To access preferential treatment under KAFTA, you will need a document called a 'certificate of origin'.

Four steps to using KAFTA

Step 1: Work out the tariff classification of your goods

Step 2: Understand how your goods will be treated under KAFTA

Step 3: Work out whether your goods meet 'rules of origin' requirements

Step 4: Certify your goods with a certificate of origin

Step 1: Work out the tariff classification of your goods

Key question: What goods am I exporting or importing?

The first step in working out how KAFTA treats a particular good is correctly identifying that good.

In KAFTA, goods are identified under an internationally-recognised system known as the Harmonized Commodity Description and Coding System, commonly referred to as the harmonised system (HS). The HS is a classification system of approximately 5,000 six-digit product categories. Typically, each country further subdivides the six-digit HS product categories into eight-digit or more tariff lines so they become more specific (Australia uses eight-digit tariff codes and Korea uses 10-digit codes).

Classification

There are a number of ways to find out the HS Code that applies to your product:

- For imports to Australia, use the working tariff provided by the Australian Customs and Border Protection Service (ACBPS), which lists all tariff classifications under Schedule 3 of the Customs Tariff Act 1995.

- For exports to Korea, use the Korean Customs Service Tariff Database Inquiry to search for your product by name.

Advance rulings

If you're still not sure about the HS classification that applies to your goods, it is a good idea to get an 'advance ruling'. Advance rulings are made by Customs and are an official ruling on the tariff classification of a good. This official ruling them becomes binding.

Advance rulings can be about the good's classification, origin or value and are valid for a specific period, such as three months or a year.

Under KAFTA, Australia and Korea must provide written advance rulings if requested by importers, exporters or producers, giving greater certainty to businesses.

Advance rulings can cover the HS classification applicable to your goods, the method the relevant customs authority will use to assess the value of your goods or whether your goods are considered 'originating' for the purposes of KAFTA (see Step 3).

Australian exporters should contact the Korea Customs Service to request an advance ruling. If you are importing goods into Australia and would like an advance ruling on the classification of a good, please contact the ACBPS. For more information visit the ACBPS website.

Step 2: Understand how your goods will be treated under KAFTA

Key question: How are my goods treated under KAFTA?

Once you have the tariff code, you can work out how your goods will be treated under KAFTA. Both Korea and Australia have set out their commitments to reduce duty rates on goods in lists called 'tariff schedules'.

The schedules contain thousands of rows of tariff lines that show base duty rates. In a separate column, a code is used to show the tariff staging category.

Read the tariff schedules of either country to check how your goods will be treated. You can find these in KAFTA Chapter 2, Trade in Goods: Schedule of Tariff Commitments.

Information for exporters

If you are exporting to Korea, you will need to check Korea's tariff schedule. Korean staging categories range from '0', indicating immediate elimination, to '20', meaning gradual elimination of the tariff over 20 equal annual stages, beginning on the date of KAFTA's entry into force.

The special categories 'B', 'S' and 'E' relate to: tariffs that will not be fully eliminated ('B'); tariffs that will be fully eliminated only on a seasonal basis ('S'); and tariffs that will remain at the base rate ('E'). Details of these categories are outlined in Annex 2-A Section B: Tariff Schedule of Korea.

Special category 'R' relates to rice products, which are not covered by KAFTA.

KAFTA also allows a certain amount of some goods that would otherwise be subject to a high tariff to be imported duty-free (referred to as a 'tariff rate quota'). For example, in the first 14 years of KAFTA (up to 2028), Australian businesses are able to export duty-free ('in-quota' rate) up to 50,000 metric tonnes of fodder annually to Korea (the 'over-quota' duty rate will be gradually reduced to zero over 15 equal annual stages beginning on the date of entry into force of KAFTA.) Details of goods subject to a quota are in KAFTA Appendix 2-A-1.

Find more information on quota usage and availability on the Korea Customs Service website.

Information for importers

If you are importing from Korea, you will need to check Australia's tariff schedule. Australian staging categories range from '0', meaning immediate elimination on entry into force, to '5', meaning gradual elimination of the base duty rate over five equal annual stages. Other categories such as '8A' are outlined in Annex 2-A Section A: Tariff Schedule of Australia.

What year has KAFTA reached now?

When reading the schedules, it is important to know the year of KAFTA's operation. KAFTA entered into force in 2014, making that the first year of the agreement. The remainder of the agreement is therefore dated as follows:

| Date commencing | Year of KAFTA's operation |

|---|---|

| 1 Jan 2015 | 2 |

| 1 Jan 2016 | 3 |

| 1 Jan 2017 | 4 |

| 1 Jan 2018 | 5 |

| 1 Jan 2019 | 6 |

| 1 Jan 2020 | 7 |

| 1 Jan 2021 | 8 |

| 1 Jan 2022 | 9 |

| 1 Jan 2023 | 10 |

| 1 Jan 2028 | 15 |

| 1 Jan 2032 | 20 |

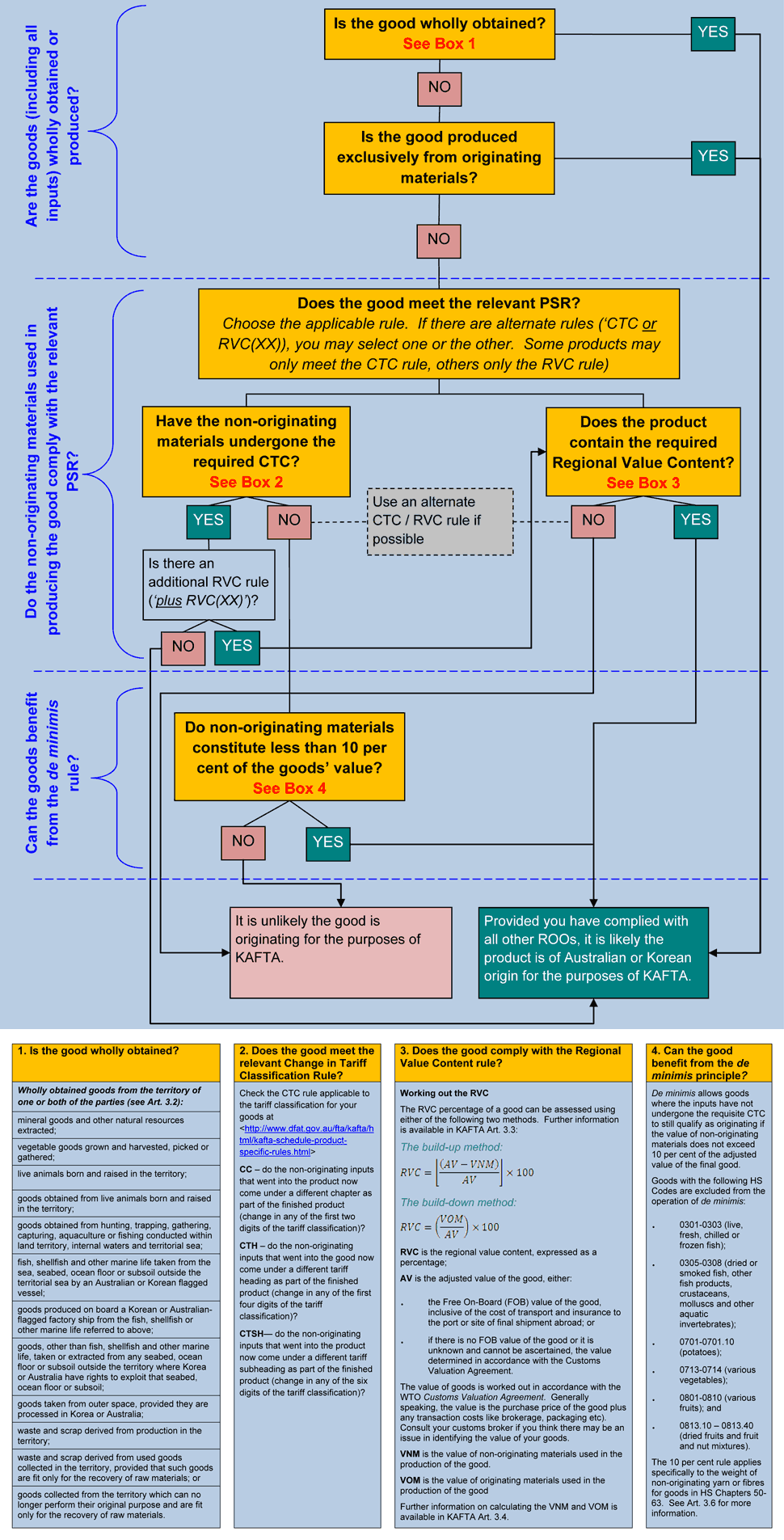

Step 3: Work out whether your goods meet 'rules of origin' requirements

Key question: Where are my goods produced?

KAFTA preferential rules of origin (ROO) are agreed criteria used to ensure only goods originating in either Korea or Australia enjoy duty preferences. Preferential ROO prevent transhipment, where goods from a third party are redirected through either Korea or Australia to avoid paying import tariffs. Any imports into Korea or Australia that do not comply with the ROO set out in Chapter 3 and Annex 3-A: Schedule of Product Specific Rules will be subject to the general rate of duty instead of the preferential rates available under KAFTA.

In general, a good will qualify as 'originating' under KAFTA if it is:

- wholly obtained or produced in Korea or Australia (or both)

- produced entirely in Korea or Australia (or both) from materials classified as 'originating' under the ROO, or

- manufactured in Korea or Australia (or both) using materials from other countries but meeting the product-specific rule (PSR) applicable to that good (see below).

Wholly obtained goods

'Wholly obtained goods' are goods that originate exclusively from one country. Typically these are agricultural goods and natural resources.

KAFTA also treats goods that are made exclusively from wholly obtained goods as being wholly obtained (Article 3.2 (l)).

Goods containing materials from outside Korea or Australia

Goods made from materials ('inputs') sourced from outside Korea or Australia may still qualify as originating, as long as they have undergone a 'substantial transformation' in Korea or Australia (or both).

PSRs set out in Annex 3A: Product-Specific Rules of Origin state the rules Korean and Australian customs authorities use to decide whether a good has undergone a substantial transformation. If your good contains inputs from outside Australia or Korea, you will need to check the applicable PSR to determine whether your good qualifies as originating.

Understanding product-specific rules

Change in tariff classification

Most PSRs in KAFTA apply a 'change in tariff classification' (CTC) approach. To qualify under the CTC rule, any non-originating inputs/materials that are incorporated into the final good must undergo a specified change in tariff classification (HS code) in Australia or Korea.

For example, pure gold (HS 7108.13) has a different classification from gold jewellery (HS 7113.19). In the process of being incorporated into jewellery, the tariff classification of pure gold changes. This means that jewellery manufactured in Australia or Korea from imported gold would count as 'originating', regardless of where the original gold came from.

Different products may be subject to different CTC rules. There are three levels of CTC rule that could apply:

- Change in chapter (CC) – change in any of the first two digits (or 'chapter') of the HS code of non-originating materials once part of the finished product. For example, importing oranges (HS Code 0805.10, from Chapter 8) and juicing them to create orange juice (HS code 2009.19).

- Change in tariff heading (CTH) – change in any of the first four digits of the HS code of non-originating materials once part of the finished product. For example, changing pure gold (HS 7108.13) to gold jewellery (HS 7113.19).

- Change in tariff subheading (CTSH) – change in any of the six digits of the HS code of non-originating materials once part of the finished product. For example, importing roasted coffee (HS 0901.21) and decaffeinating it to produce decaffeinated coffee (HS 0901.22).

Some CTC rules don't allow you to apply a CTC rule to certain inputs. For example, wheat flour (HS 1101.00) is 'CC except for Chapter 10'. Chapter 10 includes all cereals. This rule therefore means that flour produced using non-originating inputs from any chapters other than Chapter 10 will be originating.

Regional value content

A CTC is not the only way to identify substantial transformations. Some PSRs require a product to have undergone a specific amount of added value in Korea or Australia, measured by the 'regional value content' (RVC) of the good. Some PSRs provide an RVC rule as an alternative to a CTC rule; others require an RVC in addition to a CTC rule.

An RVC approach says that originating materials and processes must represent a specific proportion of the product's final value.

How to find the PSR that applies to your product

Using the tariff classification from Step 1, you can check Annex 3-A: Schedule of Product-Specific Rules.

PSRs are listed at the HS six-digit level. Using the first six digits of the relevant country-specific tariff code, find the relevant entry in the PSR list. Once you have found the relevant entry, the third column will show the PSR for that product. For example:

| HS Code | Description | PSR |

|---|---|---|

| 0710.90 | Mixtures of vegetables – frozen | CC |

| 2009.90 | Mixtures of Juices | CTH or RVC(40) |

| 8701.10 | Pedestrian-controlled tractors | CTH and RVC(40) |

In the above example, non-originating inputs into mixtures of frozen vegetables must undergo a change in chapter (change in the first two digits of the HS classification).

Mixtures of juices, on the other hand, must either have all non-originating materials used in production undergo a change in the tariff classification at the four-digit level or be made with an RVC of at least 40 per cent. Tractors must undergo the change in tariff classification at the four-digit level and retain an RVC of 40 per cent.

Further information can be found in the headnotes to Annex 3-A or by contacting your customs broker.

Other important rules of origin

There are other important factors to take into account when working out if your good qualifies as 'originating'.

The 'de minimis' rule

If a good contains a small amount of imported inputs, but those non-originating inputs don't achieve the necessary CTC once incorporated in the final good, the product may still qualify as originating. If the value of all non-originating materials used in producing the good is not more than 10 per cent of the adjusted value of the good, the product will count as originating under the de minimis rule. There are exceptions to this rule, and to qualify for de minimis classification, goods must comply with any other applicable requirements of the ROOs.

Further information can be found in KAFTA Article 3.6.

The rule of 'accumulation'

The rule of accumulation says that goods originating in one country are considered originating in the other for the purposes of KAFTA. Therefore, if Australian-originating goods were incorporated into a product made in Korea, that input would be treated as if it originated in Korea. This means that, under KAFTA, a Korean exporter to a third country, including countries with which Korea has free trade agreements, is more likely to consider inputs sourced from Australia.

'Fungible' goods and materials

Fungible goods are identical or interchangeable because:

- they have the same commercial quality

- they have the same technical and physical characteristics

- once mixed, they cannot be easily distinguished.

Examples include natural gas, grain and simple parts (for example, rivets). Specific accounting rules apply to exporters who want to show that fungible goods are originating under KAFTA.

More information is available in Article 3.7.

Rules about packaging materials, containers and packing

Packing materials and containers for shipping and transport (not retail packaging) can be disregarded when determining the origin of a good. Article 3.10 provides more information. However, retail packaging materials must be taken into account when determining origin. This means that goods packaged in non-originating retail packaging cannot be considered 'wholly obtained' and the goods will need to meet the relevant PSR.

Retail packaging materials are not taken into account in determining whether a product has complied with relevant PSRs. For example, wine bottled in non-originating bottles for retail could not be considered wholly obtained because of the non-originating bottles. However, the bottles would not be taken into account in assessing whether the wine itself had complied with the relevant PSR.

Retail packaging materials are considered in assessing the value of non-originating materials in a good for the purposes of an RVC rule, where one applies.

Further information can be found in KAFTA Article 3.9.

Indirect materials that don't qualify

Materials used to produce a good, but that are not physically part of it, are not counted in determining whether a product is originating. Examples include fuel and energy, tools, moulds, catalysts and solvents.

A full list is available in KAFTA Article 3.11.

Production processes that don't qualify

Goods will not qualify as originating if they have only undergone a simple process such as packaging, simple grinding or washing.

A full list of processes that don't count as originating is available in KAFTA Article 3.12.

Accessories, spare parts and tools

The origin of accessories, spare parts or tools presented and classified with a good will not be taken into account to assess whether a good has complied with applicable ROOs. This is provided that the quantity of accessories is what is normally supplied with those finished goods and they are not invoiced separately. However, the value of accessories, spare parts and tools is considered when assessing a good for the purposes of an RVC rule.

Shipping through a third party

KAFTA is designed to reflect modern trading practices, including using transport and distribution hubs for consigning goods. Under KAFTA Article 3.14, goods that are transhipped through a third-party (for example, Singapore) will not lose their originating status so long as they do not undergo any operation other than storing, repacking, relabelling, splitting up for transport reasons or any operation necessary to preserve the goods in good condition to be transported on to Korea or Australia.

Goods shipped through a third party must remain under customs control, or they will lose their originating status.

A simple guide to using rules of origin under KAFTA

Step 4: Certify your goods with a certificate of origin

Key question: How do I ensure I get the lower tariff rate?

Once you have gone through the first three steps and determined that your goods will qualify for preferential tariff treatment under KAFTA, you will need to complete some documentation to demonstrate this to the importing customs agency. This documentation is a certificate of origin (COO).

It is up to the exporter or producer to ensure a COO is prepared. This is known as self-certification. Australian exporters have the option of obtaining a COO from Australian accredited body under Australia’s Free Trade Agreement Certificate of Origin (FTA CoO) Recognition Scheme. See How to obtain a Certificate of Origin for more information.

Charges will apply for Certificates of Origin and may vary depending on authorised body.

If you want to prepare the COO yourself, KAFTA Annex 3D provides a model COO (see also the documents section below).

COOs can apply to a single shipment or multiple importations of goods of the same description that occur while the COO remains valid. COOs remain valid for at least two years.

Exporters or producers must maintain all records necessary to demonstrate a good's origin for five years after signing a COO. KAFTA Article 3.22 provides further detail on record-keeping requirements.

Waiver of certificate of origin

A COO will not always be required. For certain goods, Australia or Korea have waived the requirement altogether. Neither country will require a COO for goods where the total customs value is less than A$1,000 (for Australia) or the equivalent of US$1,000 (for Korea). KAFTA allows both countries to raise this threshold as required. You should check with the relevant importing customs for more up-to-date information (see contacts below).

Verifying the information in a COO

Customs authorities may occasionally need to verify the information contained in a COO. The approach they follow for this is outlined in KAFTA Article 3.23. Verification activities may involve:

- requests for information from the authorised body (ACCI,Ai Group or IECS), the importer, the exporter or the producer

- requests for information from the exporting customs administration, or

- a request to visit the exporter's or producer's premises or factory.

If information is requested, an importer, exporter, producer or authorised body has 30 days to respond. When a visit is requested, an exporter or producer should provide written consent within 30 days of receiving the notification.

Appeal procedures

If you are unhappy with a decision made by a customs administration at any point in seeking preferential treatment under KAFTA, you may be entitled to appeal that decision under KAFTA Article 4.8. You should consult your customs broker and/or legal adviser if you would like to pursue an appeal.

Disclaimer

DFAT does not guarantee, and accepts no liability whatsoever arising from or connected to, the accuracy, reliability, currency or completeness of any material in this website or any linked Australian Government website. Users of this website should exercise their own skill and care with respect to the information and advice on this website.