AN INDIA ECONOMIC

STRATEGY TO 2035

CHAPTER one The Macro Story

Summary

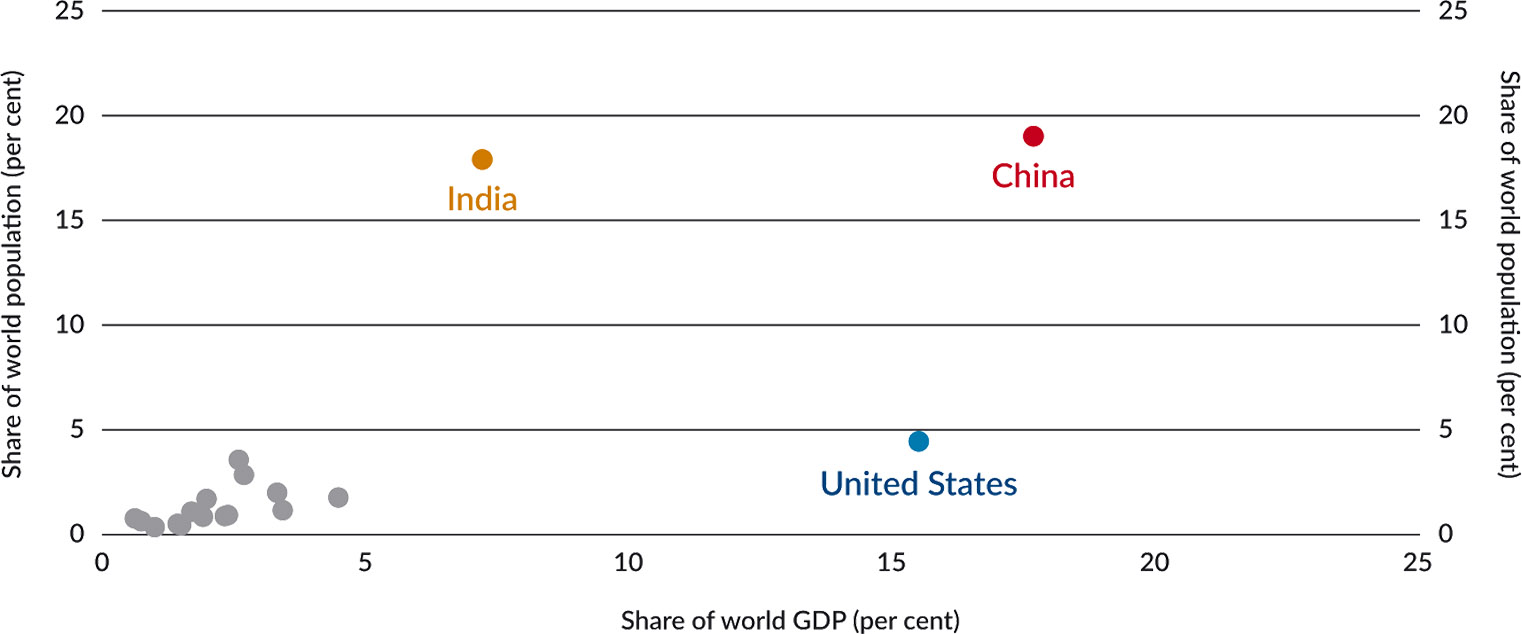

- India's economy is of global importance. It has a large and young population and an open and democratic political system. It is already the third largest economy and contributor to global economic growth, yet there is considerable untapped potential. With more than a sixth of the world's population, India produces only 7 per cent of the world's output.

- India has enjoyed a step up in growth rates over the past few decades supported by reform efforts and the expansion of its aspirational, consumer class. This report assumes a growth rate of 6–8 per cent annually over the next two decades, underpinned by productivity improvements.

- Given the challenges of policy making in such a large, diverse country with a federal structure of government, reforms will likely proceed incrementally and be politically opportunistic. Both the central and state governments have important roles to play. Making the most of India's demographic advantages will require labour market reforms, measures to improve education and skills and significantly improving women's participation in the economy. Constraints on investment and infrastructure pose a challenge, while India's services-oriented growth path will take it into uncharted territory.

- India's economic progress will not be linear. It will be subject to structural shifts and will be shaped by technological and environmental disruptions.

Outlook for the Indian economy to 2035

India's economic potential and importance

India's growth path will be driven by how effectively it harnesses and rewards the efforts of its greatest natural asset – its people. India has the second largest population in the world with more than 1.3 billion people. Of India's 29 states and 7 union territories, 18 are home to more people than Australia. India's largest state, Uttar Pradesh, is bigger than Brazil, the world's fifth most populous country.1,2 Within the next decade India's population will overtake China's to become the world's largest. By 2035, the United Nations projects that India's population will have reached almost 1.6 billion people, on its way to a peak of almost 1.7 billion by the early 2060s.

India is the world's third largest economy measured in purchasing power parity (PPP) terms and, on some measures, will be the fastest growing large economy in the world in the coming years (Figure 2).

Figure 2: Shares of world GDP and population (G20 countries)

Source: International Monetary Fund. World Economic Outlook - April 2018. International Monetary Fund; 2018.

Note: GDP is in purchasing-power parity terms. Data refers to 2017.

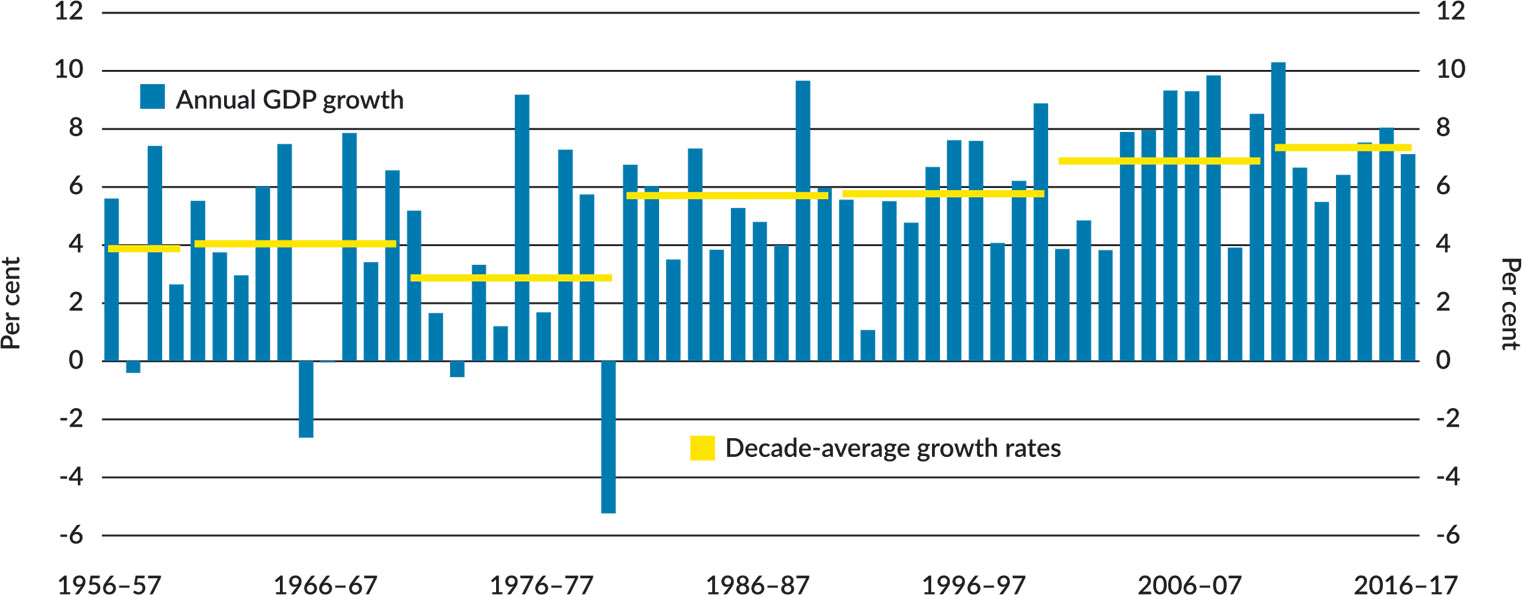

India's population has benefited from this strong economic performance. India's steps towards liberalisation and openness in the 1980s, which accelerated in the 1990s, saw India's GDP growth rise from an average annual rate of less than 3 per cent in the 1970s (the so-called 'Hindu rate of growth') to over 7 per cent in recent years (Figure 3).

Figure 3: India's GDP growthi

Source: 1) The World Bank. GDP growth (annual %). World Bank national accounts data and OECD National Accounts. The World Bank; 2018. 2) International Monetary Fund. World Economic Outlook - April 2018. International Monetary Fund; 2018. 3) Ministry of Statistics and Programme Implementation (ID). Summary of macro-economic aggregates at constant prices. New Delhi ID: Government of India; 2018.

Note: Data in India fiscal years (April to March)

Since 1970, India's real GDP per capita has increased fivefold. As a result, millions of people have been lifted out of poverty. Key development indicators such as infant mortality and life expectancy have steadily improved.

These trends have contributed to the creation of a substantial and aspirational consumer-class that, since household consumption accounts for 60 per cent of India's GDP3, is an important source of optimism for growth in the Indian economy.

Baseline scenario

Under even moderate policy progress, the Australian Treasury's long term projection framework projects that over the next two decades (and beyond) India can maintain the relatively high economic growth required to lift its share of global output.

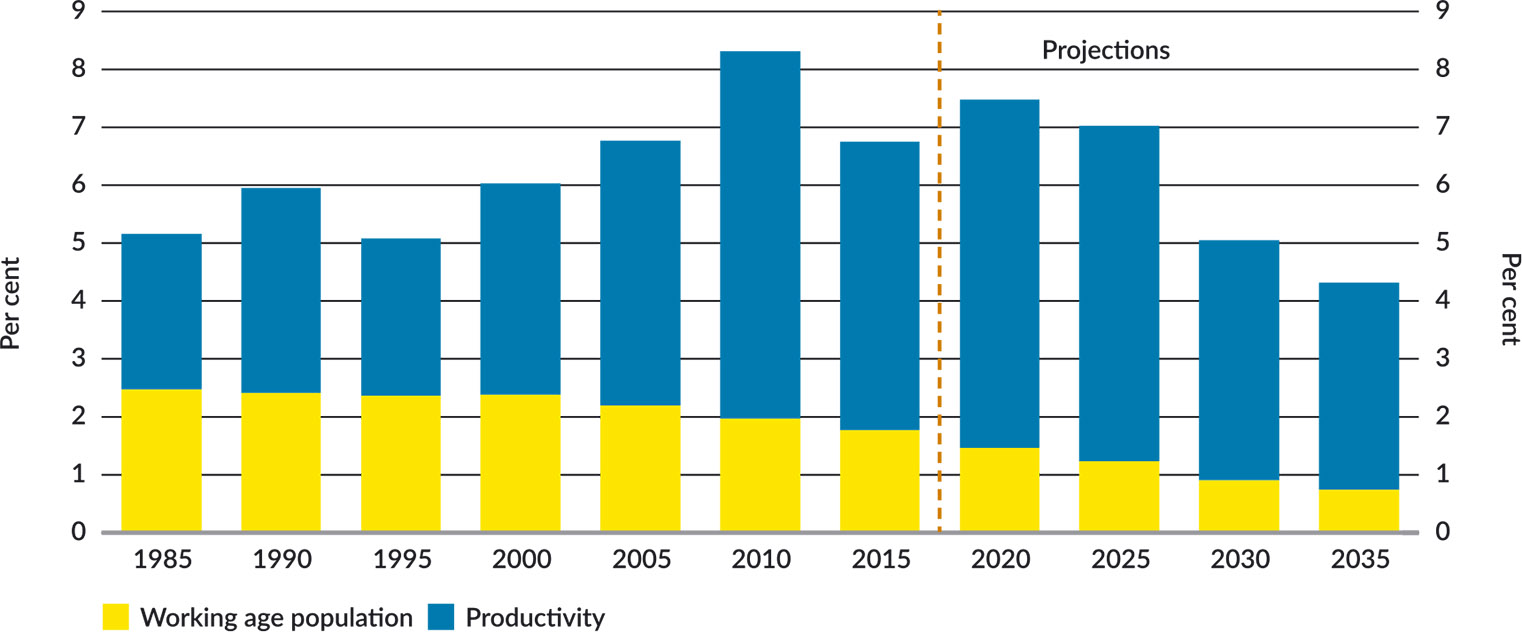

Under Treasury's projections, India will enjoy an average of around 6 per cent annual growth over the next two decades.ii As population growth continues to slow, improved productivity will remain the critical driver of GDP growth (Figure 4). Based on the incremental reforms outlined in the next section, this Strategy judges India is likely to grow at 6–8 per cent annually to 2035.

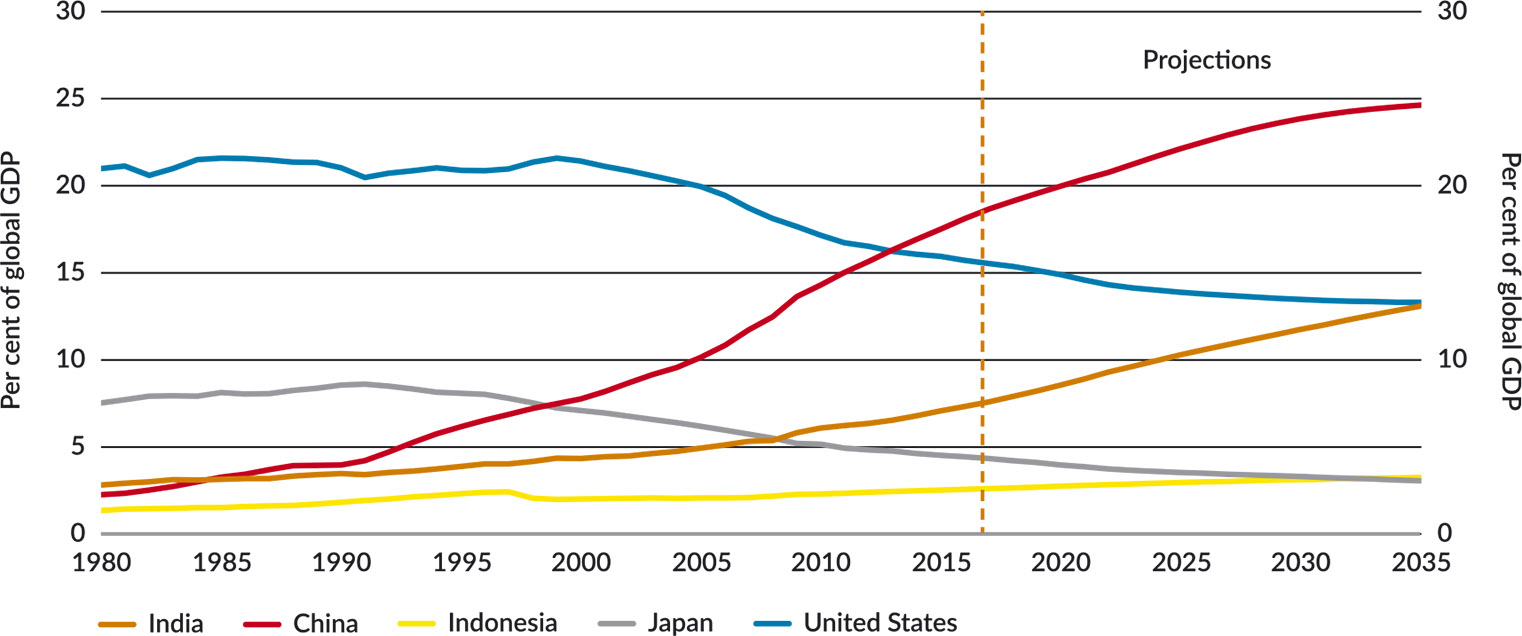

India's success will have significant implications for its international economic and strategic weight. In 2035, the global economy is likely to be increasingly weighted towards Asia, as India, China and the ASEAN economies catch up to slower-growing advanced economies. Even with an average annual growth rate of only 6 per cent, India's economy would be more than two times larger than it was in 2017. In PPP terms, India's share of the global economy will likely increase from 7 per cent in 2016 to around 13 per cent (Figure 5), making it one of the major poles of global economic power and on par with the United States.

Figure 4: Drivers of India's long term growth

Source: 1) International Monetary Fund. World Economic Outlook - April 2018. International Monetary Fund; 2018. 2) Treasury (AU); The Commonwealth of Australia; 2018

Note: Years in Figure 4 refer to five year periods ending in that year. GDP is in PPP terms.

Figure 5: Share of world GDP projections (PPP)

Source: 1) International Monetary Fund. World Economic Outlook - April 2018. International Monetary Fund; 2018. 2) Treasury (AU); The Commonwealth of Australia; 2018

Incremental reforms are likely, which will boost growth

In recent years, a greater recognition in India of the urgency for reforms to lift productivity has led to important policy achievements, including implementation of a national GST in 2017. As well as simplifying the tax system the GST sets new precedents for cooperation among the states. Future reforms will likely proceed incrementally. Both the central and state governments have the political appetite to do more, and both levels of government have important roles to play. The Central Government has direct control over several important areas, including the financial sector, [see Chapter 10: Financial Services Sector], international trade [see Chapter 16: Trade Policy Settings] and investment policy [see Chapter 2: The Investment Story].

India's state governments control crucial elements of the business environment [see Chapter 14: A Collection of States]. The Central Government has fostered a political dynamic in favour of reform, which will see uneven progress between states. Organisations such as NITI Aayog have used initiatives like competitive federalism to help states recognise the need for, and speed up the pace of, reform.

Weak capacity, at both the central and state level, to implement challenging policy changes is a key constraint. Attempts to circumvent the 'licence Raj' by moving regulatory approval systems online will improve the business environment in some areas.

Recently enacted fiscal targets and formal guidelines for monetary policy will also continue to support a favourable environment for growth. Macro stability through improvements in external indicators such as current account, foreign exchange reserves and inflation have also helped. However, fiscal pressure continues to pose a risk for many state governments, where borrowing has increased rapidly in recent years and the scope to increase debt and expenditure appears limited.

India's economic reform agenda must address three themes: its growth model and international openness, its workforce, and building the infrastructure to improve productivity.

India's growth model

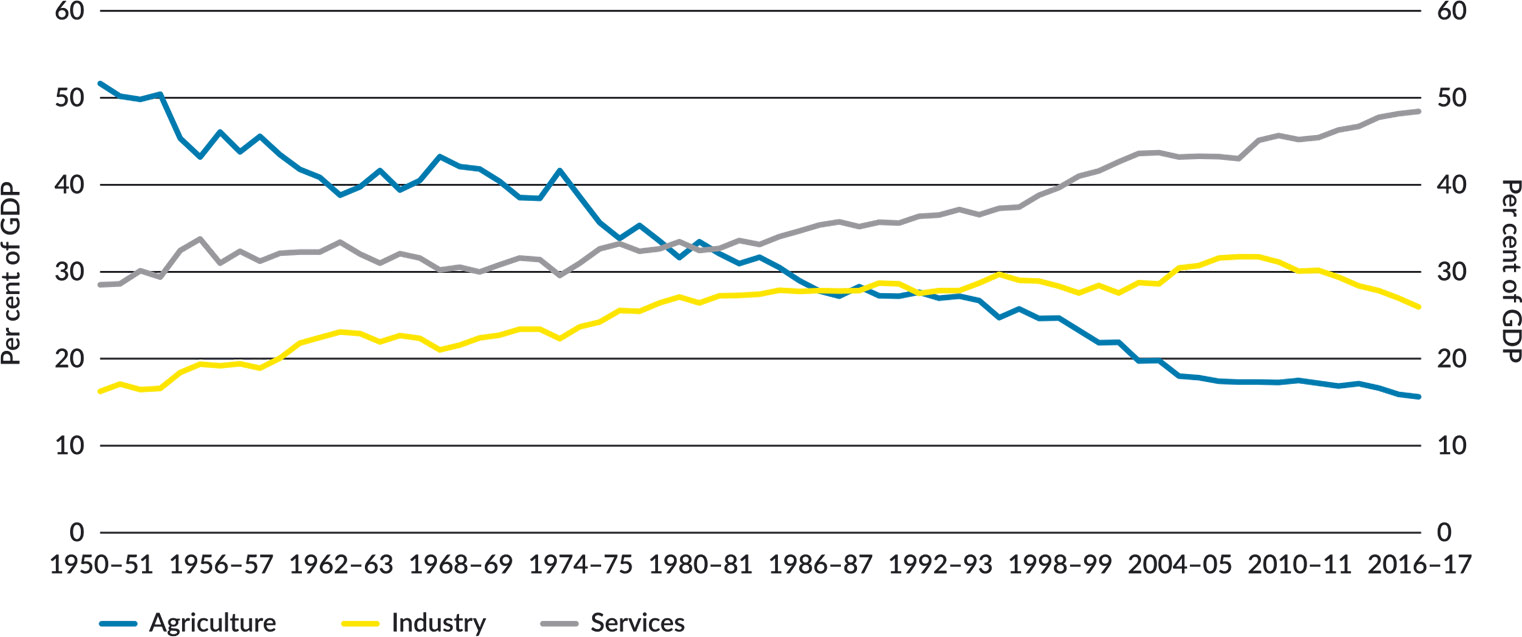

Like other emerging economies, India's growth has been marked by major shifts in the structure of its economy, most notably away from low productivity agriculture (Figure 6).

Figure 6: Sectoral shares of the Indian economy

Source: 1) CEIC Asia Database | CEIC [Internet]. Available from: https://www.ceicdata.com/en 2) Treasury (AU); The Commonwealth of Australia; 2018. 3) Ministry of Statistics and Programme Implementation (ID). New Delhi ID: Government of India; 2018

Note: Data in India fiscal years (April to March). Data prior to 2011–12 use Treasury calculations based on discontinued series.

The shift away from agriculture and strong growth in services is not unusual for a developing economy like India. What is less common is the limited role that manufacturing has played in India's development. For a typical developing economy, manufacturing drives growth and employment in the early development phase before giving way to services. For many East Asian economies, this last stage typically has occurred at much higher levels of development than in India.4

However, in many parts of South Asia, the services sector has grown ahead of manufacturing. In the traditional growth model, the services sector in developing economies is considered to be of lower productivity than manufacturing.5 In South Asia, and particularly in India, the reverse has been true. The level of India's services productivity is comparable with China and Thailand, countries with substantially higher GDP per capita. As a result, India's early shift to services has supported, rather than hindered, rapid growth.

Policy settings have supported the dominance of services

The strong expansion of India's service sector has been enhanced by a series of reforms introduced by the Indian Government through the 1990s and early 2000s. Notable reforms included financial market deregulation, a relaxation of foreign ownership regulations and moves to increase competition in a wide range of service industries. Along with the relatively high cost of capital, policy choices also appear to explain India's relative underperformance in manufacturing. Burdensome regulations – including outdated labour laws and complex land acquisition regulations – have been particularly onerous for manufacturing.

India's services success extends to exports, where a range of Indian services are globally competitive, particularly in information and communication technology and in back-office processing tasks. This reflects India's comparative advantages: a relatively low-cost workforce with a small high-skilled component, many of whom are English-speaking.

While India's services sector output has grown substantially, services sector employment has been far more modest. This has meant that a relatively small proportion of India's population has seen direct benefits. The more large scale employment the services sector can provide India, the greater the benefit for India's development.

Over coming decades, the services share of the economy is likely to gradually continue rising and the share of manufacturing stabilise. As incomes rise, the demand for consumer goods and services is expected to grow strongly, creating opportunities for domestic manufacturing. Global manufacturing firms are also likely to be attracted by India's large and growing consumer class and its relatively low operating costs.

International openness

India's structural transformation towards higher value added production would be aided by further moves to open the economy. Historically, India's size and the appeal of self-sufficiency has encouraged a degree of insularity. While the trend is positive, India's openness to trade remains among the lowest in Asia6 [see Chapter 16: Trade Policy Settings]. While India is unlikely to pursue an export-oriented growth model to the same extent as East Asia, greater openness would enable India to leverage its comparative advantage in labour intensive production, encourage innovation and lift productivity.

Greater openness to foreign investment would also support growth by providing additional sources of capital and technology [see Chapter 2: The Investment Story].

India's workforce is an opportunity and a challenge

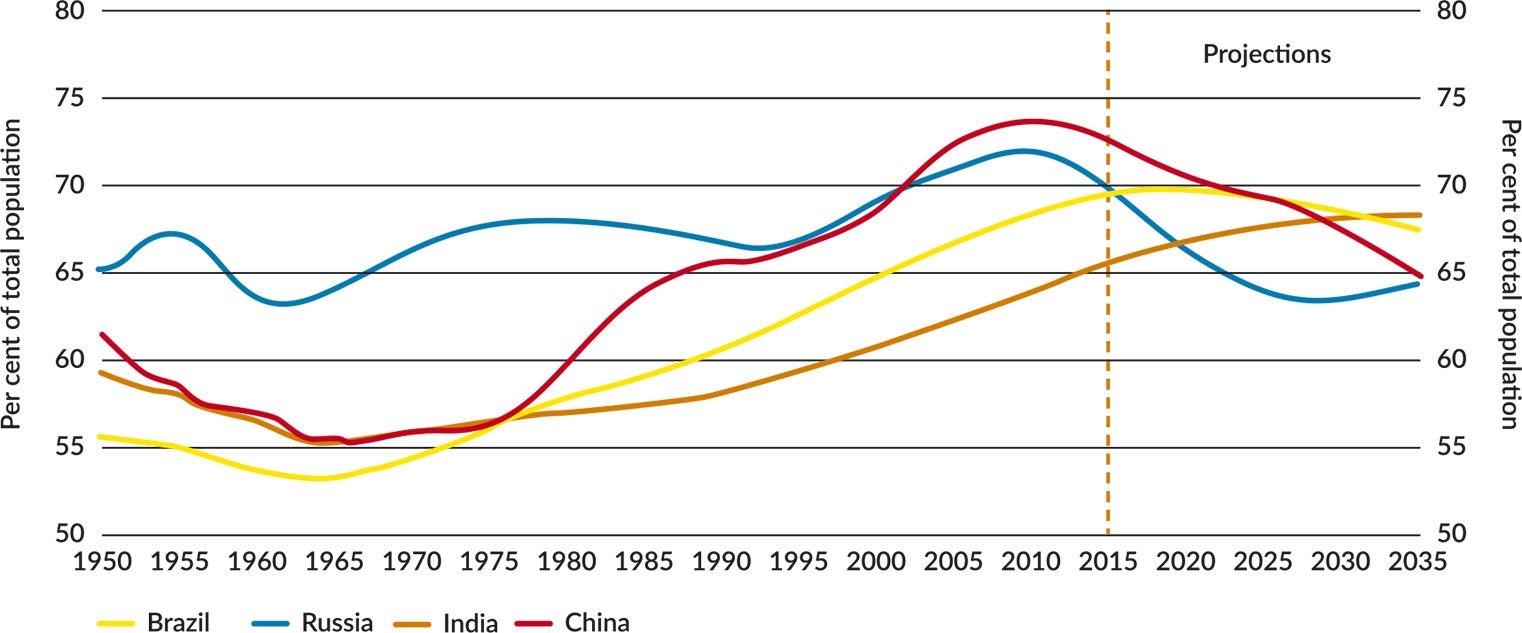

India has a great economic opportunity provided it can create an environment that supports education, training and job creation for the millions of young Indians set to enter the labour force. Over the next two decades India's working age population is predicted to increase by almost 200 million, to over one billion, to become the world's largest.1 While the rate of increase is expected to slow, the working age share of the population will continue to rise out to 2035 (Figure 7). The working age populations in southern states will peak by around 2020 but further increases in workers are expected to come from the northern states for decades to come.7

Figure 7: BRICiii working age population shares

Source: United Nations. World Population Prospects 2017 [Internet]. United Nations; 2017. Available from: https://www.un.org/development/desa/publications/world-population-prospects-the-2017-revision.html

Generating productive jobs

India's human capital formation lags many high growth East Asian countries. Firms operating in India cite access to skilled labour as a key constraint to growth. Though rising, India's working-age population had on average just over seven years of schooling in 2015. Current government initiatives are moving in the right direction, but India will need further substantial investment in its education system to make the most of its people [see Chapter 3: Education Sector].

Capitalising on a skilled workforce will require India to increase women's workforce participation and generate more productive jobs. SMEs employ around 40 per cent of India's workers.8 They make up a disproportionate share of India's economy and remain relatively inefficient, low skilled and rural-based. SMEs account for more than 80 per cent of industrial firms compared to 65 per cent in Indonesia and 25 per cent in China. However, across all sectors, India's smallest firms are only 25 to 65 per cent as productive as their peers across Asia. Firms that employ more than 200 people in India tend to be as productive as comparable firms across Asia. The preponderance of SMEs is a factor holding back India's productivity.

In part due to the dominance of SMEs, 90 per cent of Indian workers are either in the unorganised sector (self-employment or in enterprises of fewer than 10 workers) or are informal workers in the organised sector. The low rate of formal employment reduces job security and access to employer provided social security benefits for those workers.

Urbanisation

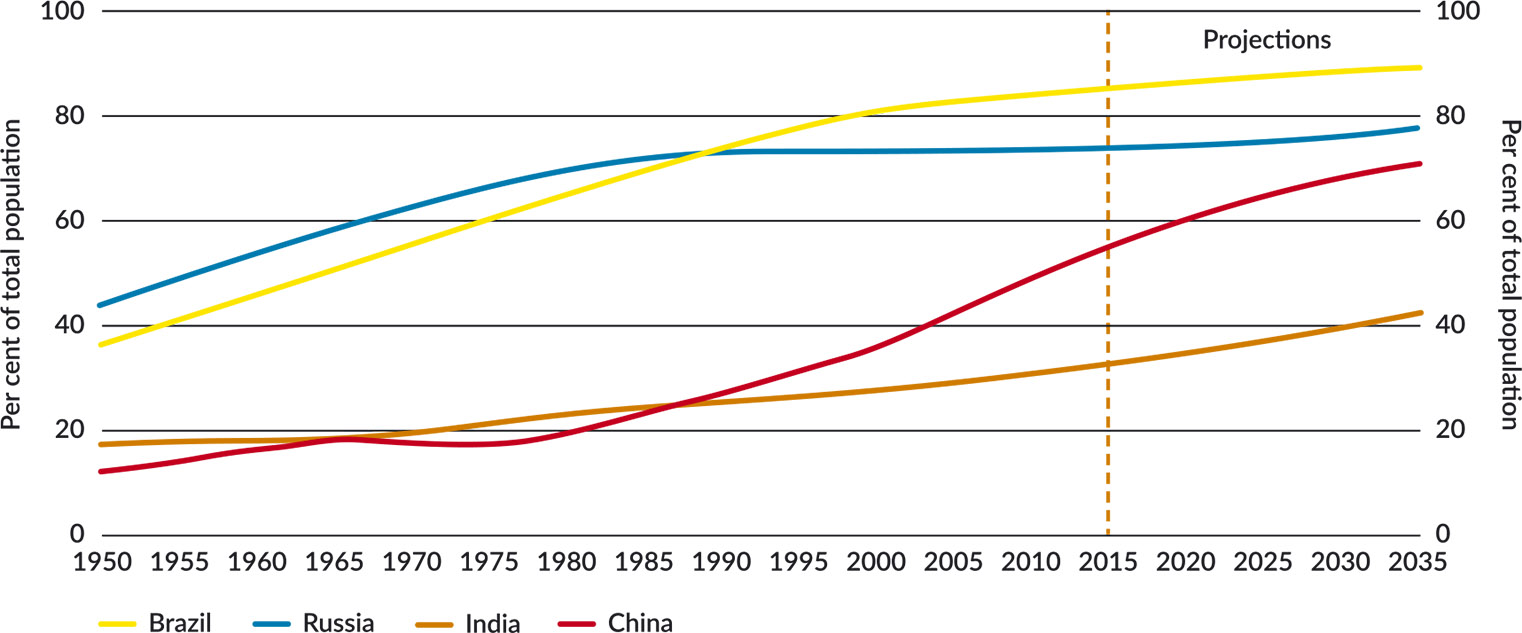

Urbanisation is driving a shift in India's workforce from lower productivity (agriculture) to higher productivity sectors (services and industry). Since 1950, the proportion of Indians living in urban areas has almost doubled, reaching 33 per cent in 2015. However, India's urbanisation rate remains low compared to other emerging economies (Figure 8). The United Nations projects that India's urbanisation rate will rise to 42 per cent by 2035, lifting the urban population from 64 million in 1950 to 640 million.9

Labour market reforms

Reforms to India's complex labour regulations would likely reduce informality, lift productivity and attract investment. There are roughly 45 national and 200 state laws governing labour relations which impose cumbersome requirements on businesses. As in other countries, labour market reform is a sensitive issue and wholesale changes will be difficult. However, attempts at reform at both the central and state level have been seen in recent years. As India's economy grows and firms look to expand their workforce more firms are likely to be affected by labour regulations and pressure to reform them may grow.

Figure 8: BRIC urbanisation rates

Source: United Nations. World Population Prospects 2014 [Internet]. United Nations; 2014. Available from: https://www.un.org/development/desa/publications/wesp2014.html

Strong investment will be needed to sustain growth

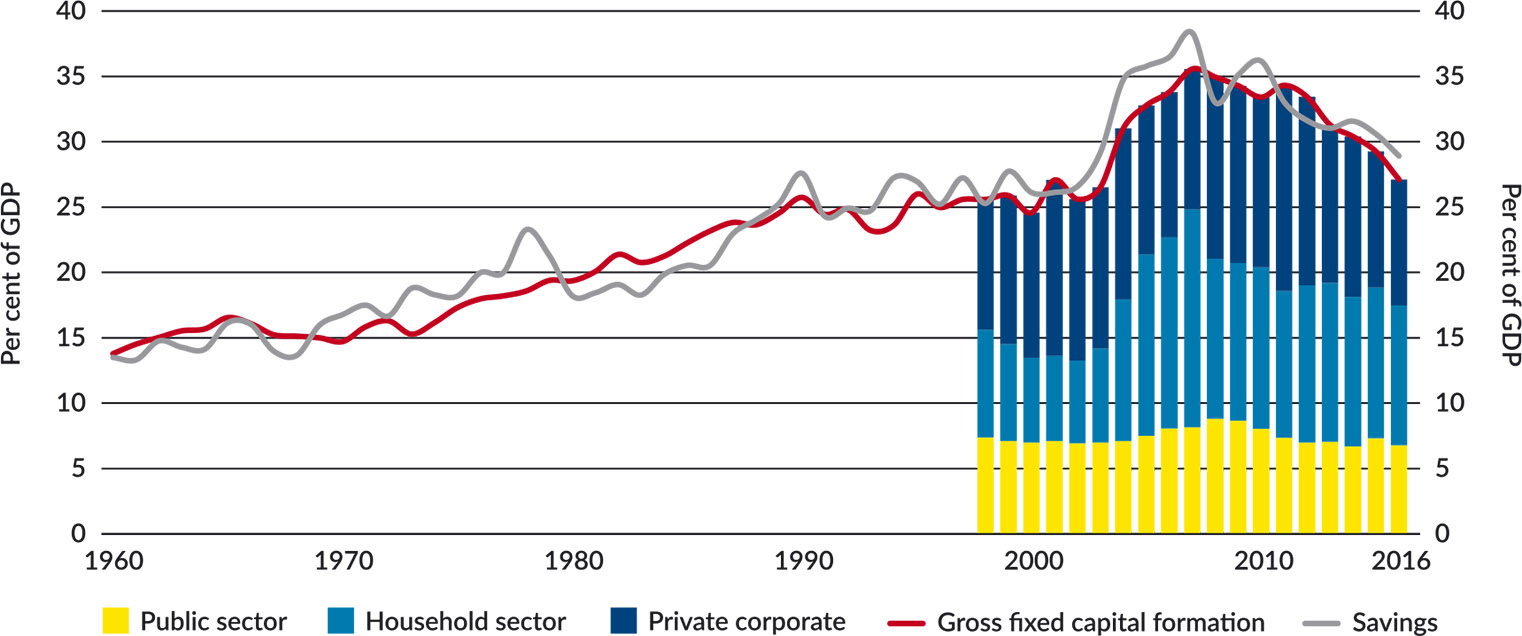

To achieve high growth in the coming decades, India will need to sustain strong investment. Capital in India has traditionally been mobilised by raising domestic savings and investing it in productive assets.

India's investment and savings rates, as a proportion of GDP, have fallen in recent years (Figure 9). Private investment has started to shrink – contracting by 22 per cent between 2014 and 2016 according to World Bank data. Turning this trend around will require a supportive environment for business, an efficient and innovative financial sector and dealing with the non-performing assets (NPAs) that have impaired new lending and weigh heavily on India's dominant public sector banks [see Chapter 2: The Investment Story].

Investment into infrastructure that enables growth, particularly in transport, energy and communications, is critical to India's prospects. How well India can deliver on this will go a long way to determining its growth path. For example, some 240 million Indians still lack access to electricity.10 The Indian Government has estimated that its infrastructure gap over the next decade will be over USD1.5 trillion.11 As a result, the central and state governments are developing new financing models to attract private, and particularly foreign, capital.

Improving India's business climate will also help increase investment. The Indian Government's renewed focus on achieving reforms has contributed to India's jump of 30 places in the 2018 World Bank's global ease of doing business ranking.100 Important areas that continue to affect the business environment in India include the effectiveness and pace of the judicial system, and business licencing regulations. Improving India's business climate will take time, but will be important in shifting focus toward opportunities available in India [see Chapter 15: Understanding the Business Environment].

Figure 9: Investment and Savings to GDP

Source: World Development Indicators | DataBank [Internet]. 2018. Available from: http://databank.worldbank.org/data/reports.aspx?source=world-development-indicators

Complex land regulations also constrain investment and growth by limiting the sale, lease and conversion of land and creating uncertainty around the true price of land holdings. The dominance of inefficient SMEs is likely to continue until more land for industrial use in urban areas is made available by local governments and it is easier for industrial firms to expand their land holdings. Existing land regulation ties farmers to their land, hinders urbanisation and the transfer of labour to more productive sectors. States which move to rationalise land markets will improve their growth prospects.

Structural shifts and sources of disruption out to 2035

A strategy out to 2035 must anticipate volatility. While deep-set structural drivers enable us to project the broad direction of India's growth, it is unlikely to be linear or evenly distributed.

This is partly due to the inherent uncertainties associated with forecasting over such a long horizon but also the complexities of India's economic model and reform path. India's economic progress will be influenced by an accelerating global rate of technological change and by trends and events in ways we cannot foresee.

Potential structural shifts

This report highlights three potential structural shifts that could change the composition, size and shape of India's economy out to 2035, including productivity, labour inputs and domestic consumption.

Future of work

Technological advances in automation and digital connectivity are changing how labour markets and businesses operate, including in India. Technology has always shaped the workplace, but the current and forecast rate of global technological change is faster than ever before, and increasing.

This will offer some positive outcomes for India. Automation technologies such as robotics and artificial intelligence can increase productivity and help Indian companies compete internationally. New jobs will be created, including in information systems to build tools for managing workers alongside machines. While India's private sector is yet to make a significant global impact in artificial intelligence development, its strong IT base gives it potential to do so.

Concurrently, digital connectivity will contribute to the decentralisation of economic activity away from large corporations, seeing production become more fragmented. This will support more flexible employment and enable more workers to participate as micro-entrepreneurs. By connecting workers and firms, digital job matching platforms can link developing economies, like India, with consumers and investors in rich countries underpinning economic convergence. This will lead to more digitally enabled services trade, new markets for exporters and potentially cheaper inputs to Australian companies. The question is whether India's high proportion of SMEs, currently a drag on productivity, will become an asset.

The future of work will also have negative effects on India's economy. Decentralisation will create more precarious and irregular forms of work and weaken job security in the formal sector. Automation has the potential to stifle India's exports because trading partners could use automation to onshore services and resources. Automation also risks displacing workers who perform routine or processing tasks,12 impeding India's net job creation, which is already growing slower than its working age population.

India's uptake of automated technologies is likely to be slower and proportionally smaller than in other economies. Low wages and abundant labour weakens the demand for it. But as with everything in India the numbers are still big. Some 125 million Indian employees are currently working in automatable areas.13 Of these, women will make up a disproportionately large number. Workers in India's manufacturing and transport/warehousing industries are most at risk of displacement, along with middle class jobs in India's back-office processing operations.

So while India's economy will continue to grow, jobs could become less secure. A scenario with more irregular forms of work would reinforce inequality while also placing a greater onus on the adequacy of social safety nets such as cash transfers. Indian policy makers are aware that managing these risks rests on equipping workers with sufficient education, skills and access to digital infrastructure. The challenge lies in developing an agile workforce and providing new skills quickly.

Poverty and equality

India's economic progress will be defined by how its growth is distributed.

As India's economy has grown every year in the last 35 years, the share of India's population living in extreme poverty (USD1.90 a day equivalent) has fallen by 30 per cent.4 While this is to be celebrated, extreme poverty in India remains high (21.2 per cent). Most poor – some 80 per cent – live in rural areas.14 By 2035, if current trends continue, extreme poverty will fall to 9.5 per cent of the population, around 150 million people.

Sitting just above the poverty line is a large low-income bracket, many of whom are rural labourers. Mobility for those rising from poverty to low income is greater than from low income to high income. At the same time, downward mobility is also relatively high. Many families in the low-income bracket have little to no accumulated wealth and are vulnerable to shocks and falling back into poverty.

So while Indian wealth is growing faster than the global average, the distribution of this wealth remains relatively narrow. India is one of the most unequal economies in the world and the gap between rich and poor has increased over the last decade. India's richest 1 per cent earn 22 per cent of all income13 and have 58 per cent of the country's wealth.14

Together, these two factors – poverty and inequality – influence the structure of India's economy in three ways. First, the acute hardship and deprivation of large scale poverty mean India will continue to have a significant unmet need for basic services, such as water and sanitation, energy and health care. Second, poverty and inequity sharpen political sensitivities and shape the political space for economic reforms. A primary objective of India's reform program is to lift basic incomes and many of the Indian Government's market interventions, from price controls to tariffs, are designed to minimise social disruption amongst its poorest constituents. Third, inequality constrains growth, limiting the potential for consumption-led growth and discretionary spending.iv

Although Australia does not have a bilateral aid program with India, Australia is well placed to work with India to reduce inequality and lift people out of poverty. As outlined in the sectoral chapters that follow, this includes working with India to provide basic services, lift incomes in rural areas and improve productivity in India's large and inefficient agricultural sector. Australia can work with India to deliver education and training, health care and access to basic infrastructure. Australian resources and expertise can power India's development. Engaging with India on policy frameworks and regulatory settings can better connect India with international value chains and markets.

Alongside these efforts, Australia's South Asia Regional Development Program should continue to support policy dialogue, institutional and regulatory reforms in critical sectors such as water, agriculture, energy, infrastructure and trade through the Sustainable Development Investment Portfolio and regional trade and infrastructure connectivity activities across South Asia, including in India. These should focus, where possible, on priority states identified in this Strategy [see Chapter 14: A Collection of States].

Gender equality

India's economy has more to gain by achieving gender parity than any other in the world.

Out to 2035, on current participation rates, women will represent one of the largest underutilised economic forces in the country. The extent to which India can achieve progress on closing the gender gap in employment, education and in financial and digital inclusion will determine not only how equitable a society it has, but how dynamic and fast growing its economy is. According to the International Monetary Fund, raising women's participation in the labour force to the same level as men could boost India's GDP by as much as 27 per cent.17 Failure to remove barriers to women's economic participation will prevent India from reaching its potential.

The rate of women's workforce participation in India has declined over 15 years despite India's high levels of growth. India has one of the world's lowest rates of female workforce participation, 24 per cent compared with 40 per cent globally.4 Female disadvantage pervades Indian social and economic spheres. The 2017 World Economic Forum's Global Gender Gap Report ranked India 108 out of 144 countries in terms of gender parity.18

The level of women's empowerment in India is determined by variables such as geographical location, education, social status and age. But across the economy, barriers to women's employment include prohibitive social norms, women's disproportionate share of unpaid care work, a rise in household income and the absence of local job opportunities. Women who do work in India are over-represented in industries with low pay, poor labour conditions and low productivity.

The Indian Government has made commitments to boosting its female labour force participation and released policies in 2017 designed to improve paid maternity leave and childcare assistance. While changing societal norms takes time, many of India's large corporate firms are emphasising the business case for increased diversity, especially the IT sector, which employs more women in India than any other except agriculture.

These efforts build on other positive trends. The gender gap in literacy rates has narrowed by 25 per cent since 1991.4 The education gap between boys and girls has been virtually eliminated at the primary and secondary school levels and is narrowing at the tertiary level. The number of girls in India getting married before 18 has nearly halved in the last decade.19

Growing attention in India's public and private sectors to the economic benefits of workplace diversity and women's workforce participation provides an entry point for Australian advocacy and business engagement. Initiatives we pursue across our priority sectors from research and development collaboration to skilling programs, must emphasise gender equity and inclusiveness.

Sources of disruption

This report examines three non-linear trends that will affect productivity as well as supply and demand of key inputs to the Indian economy. Later chapters provide further detail on the ways water and technology will impact specific sectors.

Water scarcity

The problem of water scarcity in India is a long term challenge that will get worse before it gets better. India has around 18 per cent of the world's population but only 4 per cent of the world's water resources. Population growth, pollution and water distribution management are contributing to the depletion of available water reserves. India is therefore likely to face a water scarcity crisis before 2030, when demand is projected to outstrip supply. Many of India's large cities already face water shortages on a daily basis. Most of India's river basins could face severe deficits unless concerted action is taken, with some of the most populous regions – including the Ganga, the Krishna, and the Indian portion of the Indus – facing the biggest gap.

Water scarcity has implications for India's food and energy security. Agriculture is the largest consumer of water (around 80 per cent). Over-extraction of groundwater by farmers will see some regions exhaust their subterranean supplies within 10–15 years. While India's renewable energy agenda might alleviate the high dependence on water for energy generation, any constraints on supply to consumers and industry (which currently uses around 10 per cent of water) will adversely impact economic growth.

A water scarcity crisis in India would also have implications for stability and security in South Asia. Many cross-border agreements are under re-negotiation or dispute and India's domestic water disputes between states are just as intractable.

India has a comprehensive National Water Policy but this does not intersect with state policies and is not supported by the strong institutions, infrastructure and cross-border partnerships which are necessary for effective implementation. India also requires significant investment in infrastructure, such as water treatment plants, waste management systems and industrial water recycling technologies. The sector is crowded and coordination is challenging, as India has limited capacity to absorb assistance from multiple channels.

Technology

By 2035, technological developments will unlock growth and new markets in India in ways beyond current imagination. India may be able to leapfrog dated technologies to spur faster growth. Computing speed, device connectivity, data volumes and many other indicators of technological capability are increasing at exponential, not linear, rates.

There are many prospective technologies about which to speculate. Three examples that could change India's flow of capital and open new markets are:

E-commerce is taking off in India propelled by rising smartphone penetration and dropping data costs. Today, around 14 per cent of India's internet users shop online, compared with almost 64 per cent in China. But Indian online retail is expected to grow to 12 per cent of India's retail market, up from 2 per cent now. This rate will climb further by 2035. E-commerce will support employment, including in tier two and three cities and in micro, small and medium enterprises by increasing access to finance and revenues from export. With the introduction of the GST it should also support tax collection and curtail tax evasion – especially beneficial given India's low tax base.

Financial inclusion systems will continue to slowly transform India's economy and mobilise capital inputs. India has already introduced a universal biometric identification system (Aadhaar), initiated measures to boost the number of bank accounts (Jan Dhan) and rolled out real time payments systems (Unified Payments Interface and Bharat QR). Along with the GST, these advances will lead to greater tax compliance and revenue for the government, enable welfare spending with smaller leakages, and help combat corruption. Through electronic transfers and lower costs of managing loans, digitisation offers platforms for providing credit to micro enterprises, including in rural areas, leading to greater productivity.

The future of transport will influence India's energy and connectivity scenarios. Faster progress in electric vehicle development could lead to shifts away from liquids-driven transportation, presenting risks and opportunities to India's automotive manufacturing sector. Autonomous and electric cars, ride sharing, and other technological innovations in heavy-duty vehicles could substantially reduce oil demand and could see a trend away from private ownership of vehicles. For example, cab-hailing app based companies such as Uber and Ola have been successful in India, with about 700,000 vehicles in operation in 2017, up from 300,000 in 2015.12 India, as a major oil importer, has benefitted from the low oil prices of 2015 to 2017 which has been a boon for its current accounts. Any trends or technologies which contribute to lower global oil prices or drive down domestic demand will have a net positive effect on India's economy.

Climate change

Changing environmental conditions lead to economic, environmental and security risks. The challenge posed by climate change will deepen out to 2035. India, like Australia and the rest of the world, will need to factor climate change into long term planning and investment, including its implications for our economies and national and regional security.

For India, climate change is compounding and hastening its water crisis, with forecast changes to the monsoon patterns, rising temperatures, more intense weather events, and glacier retreat in the Himalayas. Less, and less consistent, rainfall will impact food and energy production, especially as India lacks the storage capacity to capture monsoon rains. The production of staples like wheat and rice are particularly susceptible to extreme heat and water scarcity.

An increasing frequency of natural disasters brings with it human suffering and rehabilitation costs. A growing body of evidence shows that the poor are the most affected. Disasters from climate change have the potential to push those most vulnerable even deeper into poverty and interrupt the economic mobility of millions.

Indirect risks include potentially less availability of global capital to finance India's thermal power projects, with the lenders citing climate change concerns. Companies will need to adjust to price volatility of raw materials and commodities as well as increased regulation. The impact of climate change on agriculture and livelihoods could increase the number of climate refugees.

Responses to climate change and environmental pollution will open up opportunities for Australian capabilities. This includes areas as diverse as renewable energy, sustainable cities, climate smart agriculture and infrastructure, water management and climate finance. Our shared interest in transitioning to a low emissions, climate resilient global economy should see us continue to work closely together bilaterally, regionally and multilaterally.

Outlook for the Australian economy to 2035

An Australian strategy for engagement with India out to 2035 must take account of how our own economy will evolve. We need to understand the position of both economies in order to plot their intersection.

On average, the Australian economy is estimated to grow at around 2.75 per cent annually over the next two decades, based on projections regarding population growth, participation in the workforce and productivity growth.

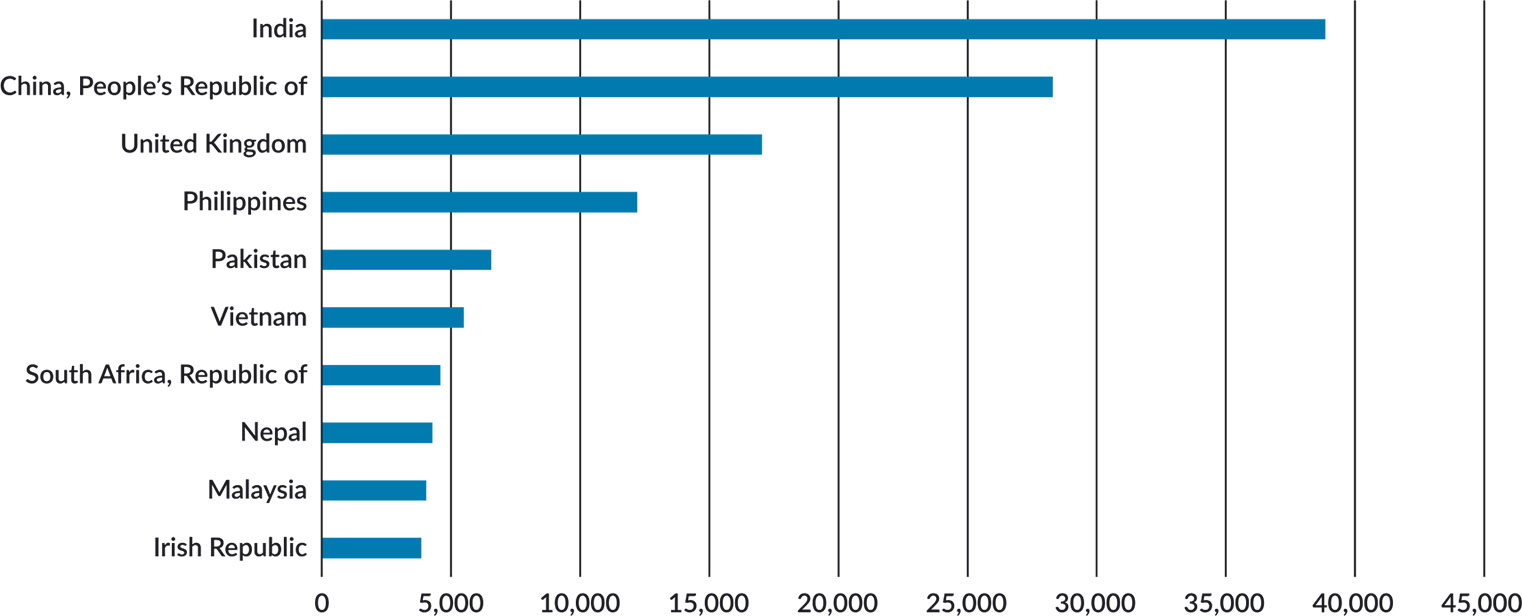

In the 2015 Intergenerational Report, Australia's population is projected to grow at around 1.3 per cent per year, slightly below the average growth rate of recent decades, to reach around 32 million in 2034–35. This projection is based on the assumptions that fertility will remain at around the 2013 rate of 1.9 births per woman and net overseas migration will continue at a level similar to recent migration intake settings.20 Of note, India is currently the largest source country of Australian immigration, making up 21.2 per cent of all immigration in 2016–17 (Figure 10).21

Figure 10: Top 10 source countries of migrants by citizenship 2016–17

Source: Department of Home Affairs (AU). 2016–17 Migration Programme Report. Canberra: The Commonwealth of Australia; 2017.

The age profile of Australia's population is also projected to change as the overall population grows. Australians are projected to live longer and continue to have one of the longest life expectancies in the world. As a result, there will be fewer people of traditional working age compared with the very young and the elderly. This trend is already visible, with the number of people aged between 15 and 64 for every person aged 65 and over having fallen over the past few decades.

Over the coming decades, the proportion of the population participatingv in the workforce is expected to decline as a result of the population ageing highlighted previously.

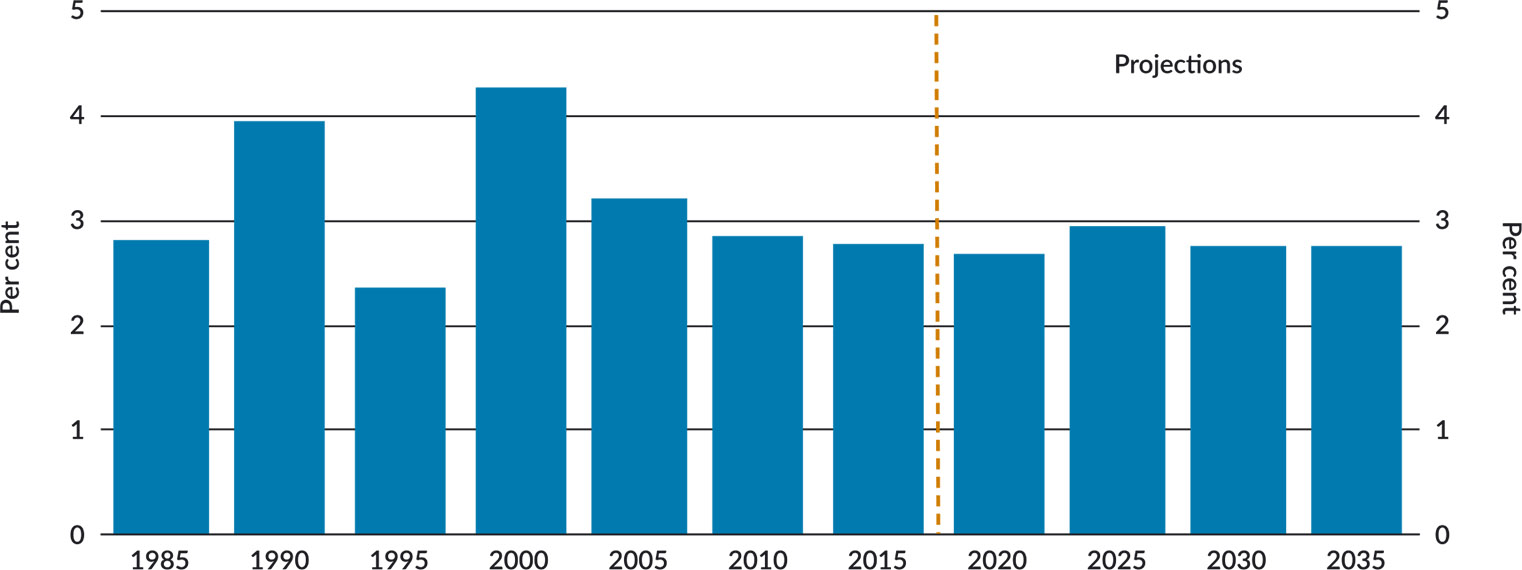

Of the three key drivers of economic growth, productivityvi has historically been the most important to Australia's economic performance (Figure 11).

Figure 11: Australia's long term growthvii

Source: 1) Australian Bureau of Statistics (AU). ABS cat. no. 5206.0; MYEFO 2017–18. Canberra AU: The Commonwealth of Australia; 2018. 2) Treasury (AU), The Commonwealth of Australia.

Note: Growth rates are average annualised growth for five financial years, 1985 represents growth from 1979–80 to 1984–85. Historical GDP growth rates have been used up to 2016–17. Australian projections use published growth rates from the 2017–18 MYEFO from 2017–18 to 2020–21, 3 per cent for the first three years after the forward estimates, then 2.75 per cent beyond. On average, over the next two decades annual economic growth is estimated to be around 2.75 per cent.

- iAnnual percentage growth rate of GDP at market prices based on constant local currency. Aggregates are based on constant 2010 USD. GDP is the sum of gross value added by all resident producers in the economy plus any product taxes and minus any subsidies not included in the value of the products. It is calculated without making deductions for depreciation of fabricated assets or for depletion and degradation of natural resources.

- iiTreasury's long term projection model is based on assumptions about productivity and working age population growth. For productivity, the model estimates each country's ‘steady state' level of productivity relative to the United States, based on an assessment of the country's competetiveness (the World Economic Forum Global Competitiveness Index, or GCI). The model then assumes that countries approach this steady state level over time. Reforms that increase a country's competitiveness, and hence its GCI score, would lead to a higher estimated steady state level of productivity relative to the United States and an upward revision to projected productivity growth. All else equal, this in turn would mean higher projected GDP growth. The working age population projections are based on those published by the United Nations.

- iiiIn economics, BRIC is an acronym that refers to the countries of Brazil, Russia, India and China, which are all deemed to be at a similar stage of newly advanced economic development.

- ivOECD analysis finds a negative and statistically significant correlation between income inequality and economic growth.

- vParticipation refers to the proportion of the population of people aged 15 years and over who are actively engaged in the workforce.

- viFuture productivity growth is inherently uncertain, so historical productivity growth is used as a guide. Labour productivity is assumed to grow at the average annual growth rate of the previous 30 years (1.5 per cent at the time of the Intergenerational Report).

- viiThe projections of the drivers of potential growth are developed using a range of assumptions and therefore are not without uncertainty. The sensitivities of economic growth to assumptions for the projection of annual net overseas migration, the participation rate and productivity growth are presented in the Intergenerational Report.